by Jeff Cody

How much did college cost when you were a student? I'll bet I can just about guess and be in the ballpark. When you were a student, it cost to go to college for three or four years what is estimated for your son or daughter to go to college for one year today. Am I in the ballpark? Joking aside, In case you haven’t noticed, the cost of attendance has changed quite a bit. In fact, with many colleges today costing more than $100,000 per year, college costs are now scary expensive.

So, what is your plan? How do you and your student intend to pay for college? Many families today are saying no to higher education and have replaced their thinking more along the lines of community college or trade school, or nothing. But the question is –Is that what you want? If there was a way for you to have your cake and eat it, too, where no matter what college costs, you could send your student off to college to enjoy the same life molding experience you encountered but doing it in a way that did NOT impact your future financial life and your retirement?

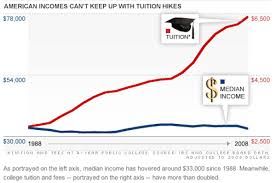

Let’s take a closer look at college inflation. College inflation refers to the long-term trend of college costs rising at a much faster rate than the general inflation rate, which is driven by factors like decreased public funding, increased administrative costs, and higher demand. For years, college costs have been rising at a rate of around double what the cost of living is, a nearly 10-fold increase compared to a roughly 3.25-fold increase in the cost of living between 1978 and 2008 according to Google.

Another factor to consider is graduation rates are increasingly longer today with most students now taking an average of 6.2 years to graduate from public universities. That begs to ask this question then about the Public vs. Private college debate: Is going to public college really less expensive?

The impact of college inflation also is dangerously significant for those who are financially and retirement minded. Below is a list of the effects of higher college costs on many middle income to upper -middle income families.

Higher costs: Over time, college tuition has risen much faster than other household expenses, with some estimates showing it has increased four times faster than housing and gas prices.

Increased student loan debt: The rising cost of college, coupled with the easy access to loans, has contributed to a significant increase in student loan debt, which nationally now is above $1.77 trillion.

Disproportionate burden: After adjusting for inflation, the average net tuition and fees paid by students have increased over the years, placing a greater financial burden on families.

Outpacing inflation: College costs have consistently outpaced general inflation, with some studies showing tuition increasing at rates up to three times faster than the cost of living.

So after reading this blog and feeling the effects of inflation, do you still believe that the best, most efficient way of saving for college and paying for it is by stuffing a 529 plan as full as possible? Did you know that every dollar you put in a 529 plan, an UGMA or UTMA, you are actually costing yourself a dollar of aid from the college or government?

Register for and attend our free educational workshop on college affordability! Just go to https://collegeplusretirement.com/workshops to learn more and register.